A T-account is a visual aid used to depict an account in a general ledger. Above the top portion of the T would be the account title. On the left-side of the base of the T would be any debit amounts; on the right-side would be the credit amounts.

The T-account can be helpful in determining the proper balance for an account or to determine the amount to be entered in order to arrive at a desired balance. I always use two (or more) T-accounts when determining how to adjust an account balance. Drawing two T-accounts reminds us that every transaction or adjustment will have to involve at least two accounts because of double-entry accounting.

A common use of T-accounts is in preparing adjusting entries (accruals and deferrals). I begin by drawing two T-accounts. Next, I note that one of the T-accounts will affect a balance sheet account. The other T-account is noted as affecting an income statement account.

As a young accountant I had to determine the effect of a new FASB standard on my employer’s financial statements. I reported on the impact on the company’s expenses in great detail. I thought I was done until the controller drew two T-accounts on a piece of paper and said, “What about the other account? You told me about the expense account, but what other account or accounts are affected. You know we have double-entry accounting!”

You might get in the habit of using two T-accounts each time you attempt to determine the proper accounting entry. It will help you see the proper amounts and the proper accounts.

A suspense account is a general ledger account in which amounts are temporarily recorded. The suspense account is used because the appropriate general ledger account could not be determined at the time that the transaction was recorded.

As soon as possible, the amount(s) in the suspense account should be moved to the proper account(s).

Example of Using a Suspense Account

An accountant was instructed to record a significant number of journal entries written by the controller of a large company. Unfortunately, there was one amount that did not have an account designated. In order to complete the assignment by the deadline, the accountant recorded the “mystery” amount in the general ledger Suspense account. When the controller is available, the accountant will get clarification and will move the amount from the Suspense account to the appropriate account.

A trial balance is an internal report that remains in the accounting department. The trial balance lists all of the accounts in the general ledger and their balances (or all of the accounts that have balances). However, the debit balance amounts are entered in one column and the credit balance amounts are entered in another column. Each column is then summed to prove that the total of the debit balances is equal to the total of the credit balances. (In a manual accounting system, the trial balance would draw attention to the errors occurring when transactions were journalized, posted, account balances computed, etc. With accounting software, these clerical errors are unlikely.)

Definition of Balance Sheet

A balance sheet is one of the five financial statements that are distributed outside of the accounting department and are often distributed outside of the company. The balance sheet summarizes and reports the balances from the asset, liability, and stockholders’ equity accounts that are contained in the company’s general ledger. The balance sheet is also referred to as the statement of financial position.

The double entry system of accounting or bookkeeping means that for every business transaction, amounts must be recorded in a minimum of two accounts. The double entry system also requires that for all transactions, the amounts entered as debits must be equal to the amounts entered as credits.

Example of a Double Entry System

To illustrate double entry, let’s assume that a company borrows $10,000 from its bank. The company’s Cash account must be increased by $10,000 and a liability account must be increased by $10,000. To increase an asset, a debit entry is required. To increase a liability, a credit entry is required. Hence, the account Cash will be debited for $10,000 and the liability Loans Payable will be credited for $10,000.

Double Entry Keeps the Accounting Equation in Balance

Double entry also means that the accounting equation (assets = liabilities + owner’s equity) will always be in balance. In our example, the accounting equation remained in balance because both assets and liabilities were each increased by $10,000.

A general ledger account is an account or record used to sort, store and summarize a company’s transactions. These accounts are arranged in the general ledger (and in the chart of accounts) with the balance sheet accounts appearing first followed by the income statement accounts.

Examples of General Ledger Accounts

Some of the more common balance sheet accounts and how they are further arranged in the general ledger include:

asset accounts such as Cash, Accounts Receivable, Inventory, Investments, Land, and Equipment

liability accounts including Notes Payable, Accounts Payable, Accrued Expenses Payable, and Customer Deposits

stockholders’ equity accounts such as Common Stock, Retained Earnings, Treasury Stock, and Accumulated Other Comprehensive Income

Some of the general ledger income statement accounts and how they are arranged include:

operating revenue accounts such as Sales and Service Fee Revenues

operating expense accounts including Salaries Expense, Rent Expense, and Advertising Expense

nonoperating or other income accounts such as Gain on Sale of Assets, Interest Expense, and Loss on Disposal of Assets

General Ledger Control Accounts

Some general ledger accounts can become summary records and will be referred to as control accounts. In that situation all of the detail that supports the summary amounts in one of the control accounts will be available in a subsidiary ledger.

Examples of General Ledger Control Accounts

A common example of a general ledger account that can become a control account is Accounts Receivable. The summary amounts are found in the Accounts Receivable control account and the details for each customer’s credit activity will be contained in the Accounts Receivable subsidiary ledger.

Other general ledger accounts that may become control accounts include Inventory, Equipment, and Accounts Payable.

Drawing Account is a contra owner’s equity account used to record the withdrawals of cash or other assets made by an owner from the enterprise for its personal use during a fiscal year. It is temporary in nature and it is closed by transferring the balance to an owner’s equity account at the end of the fiscal year. The word drawings refer to a withdrawal of cash or other assets from the proprietorship/partnership business by the Owner/Promoter of the business/enterprise for its personal use. Any such withdrawals made by owner leads to a reduction in owner’s equity invested in the Enterprise. Therefore, it is important to record such withdrawals (made by the owner) over the year in the balance sheet of the enterprise as a reduction in owner’s equity and assets.

Drawing Account Entry Example

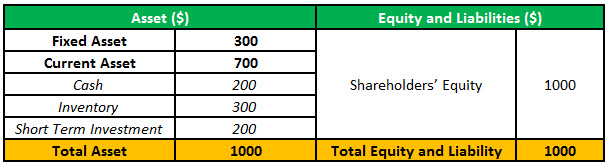

To understand the concept of the drawing account and its utility, let’s start with a practical example of a transaction in a sole proprietorship business. Assuming the owner (Mr ABC) started the proprietorship business (XYZ Enterprises) with an investment/equity capital of $1000.

The Balance sheet of XYZ Enterprises as on 1st April 2017 is as below:

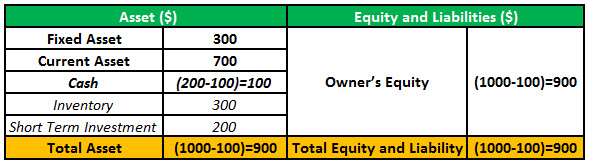

Suppose Mr ABC takes out $100 from the business for its personal use during the financial year FY18. The impact of the above transaction on the Balance sheet will be a reduction in the cash balance and in the owner’s equity capital by $100. Therefore, the Balance Sheet after the transaction will look like this:

Above demonstration is one example of a transaction, however, in proprietorship/partnership the owners generally may do multiple transactions during a fiscal year for their personal use. There is a mechanism to record such transactions and adjust the Enterprise’s Balance Sheet for such transactions where the Owner uses business resources (cash or goods) for personal use.

Drawing Account Journal Entry

Extending our discussion from initial section of the article where we have taken the example of Mr. ABC (Owner) making a withdrawal of $100 from its proprietorship business (XYZ Enterprises) for its personal use. This transaction will lead to a reduction in owners’ equity capital of the XYZ Enterprises and also a reduction in Cash Balance of the enterprise.

Since a drawing account is set up as contra owner’s equity account to record this and similar other transactions of this nature, following transactions will be recorded in drawing account. Drawing account Journal entry for the above cash transaction by owner will be recorded with a debit in owner’s and as credit in the cash account. The entries for the above transactions will be as below:

Since drawing account is a temporary account and it is closed at the end of the financial year. At the end of the financial year, the drawing account balance will be transferred to the owner’s capital account thereby reducing the owner’s equity account by $100.

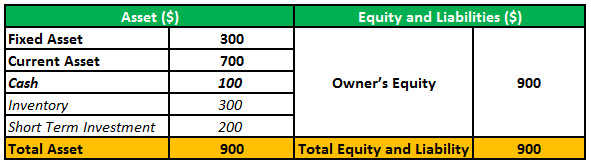

Therefore, at the end of the Year owner’s equity balance will be as below:

Also, Cash account on the asset side of the balance sheet at the end of financial year FY18 will reduce by $100 and a closing balance will be as below:

Cash= (200-Cash withdrawals) = (200-100) =$100

Therefore, the balance sheet position of XYZ Enterprises at the end of the fiscal year FY18 to include the impact of an above-discussed transaction will be as below

Summary of the Drawing Account Entry

Drawing account is mostly used in reference to proprietorship business or partnership business to record the owner’s drawing from its enterprise in the form of cash or other assets.

Its a contra owners equity account to an associated owners equity account.

It is used to record the transaction of an owner withdrawing cash or other assets from its proprietorship enterprise for personal use.

It is temporary in nature which is closed at the end of the fiscal year and starts with zero balance to record the owner’s withdrawals in next fiscal year.

It is closed at the end of the fiscal year by transferring the balance from drawing account to owners’ equity capital account.

It’s useful in keeping track of distributions made to owners in a partnership business thus helps in avoiding any disputed between partners in business.

Write-Off happens when the recorded book value of an asset is reduced to zero. Usually, this happens when the assets of the business cannot be liquidated and are of no further use to the business or have no market value.

It can be defined as the process of removing an asset or liability from the accounting books and financial statements of a company. For example, this might happen when inventory becomes obsolete or there is no particular use of a fixed asset. Generally, it is done by moving a part of or all of the balance in an asset account to an expense account. The write-off accounting though varies with the types of assets.

It usually occurs once and is not spread over various periods. A tax writes off is the reduction of taxable income. In retail companies, the common write-offs are damaged goods and in industrial companies, it happens when a productive asset gets damaged and is beyond repair.

Why Write-Off is done?

It happens mainly because of two reasons.

It helps with tax savings options for asset owners. Actions like write-off reduce tax liability by creating expenses that are non-cash in nature which ultimately results in lower reported income.

It supports the objectives of a write-off accounting accuracy.

Write-Offs Examples

Bad Debt – Bad debt can happen when a business client owes money to the company but is unable to pay back the invoice amount since the client has been declared bankrupt. The amount of debt which could not be collected is taken as a loss and the company writes it off on its tax return.

Asset Write-Offs – This happens when a company removes an account or assets from write-off accounting books. In this case, the asset’s value has gone down to zero and that is the reason for writing off the asset from the accounting records.

Accounts Receivables – In the situation of write-off accounting receivable not being collected, it is usually offset against the allowance for doubtful accounts i.e. contra account.

Inventory – In case of obsolete inventory, this can either be charged directly to the cost of goods sold or offset against the reserve for inventory which is obsolete (contra account).

Advanced Pay – When a pay advance given to an employee cannot be collected then it is charged to compensation expenses.

How Write-Off is Applicable for Banks

A bank is in the business of lending money to individuals or companies. In an ideal situation, banks expect to get back the money that they lend to other organizations, for the expansion of their business. But there are situations where the organizations fail to generate income from their operations, ends up making losses and defaulting on their loan payments.

That is why banks maintain the provision for bad debt. For banks loans are there primary assets and source of future revenue. If the bank is not able to collect a loan or there is minimal chance of the collection of a loan a then it affects the financial statements of a bank and will result in diverting resources from other productive assets.

As a result for loans that have the high probability of getting defaulted, banks use write-offs for those loans from their balance sheet.

Bank Write-off Example

Let us understand with the help of an example how a bank reports a loan in its financial statements and maintains the provision for the bad debt. Suppose a bank lends $100,000 to an organization and have 5% provision for bad debt against that loan. Once the bank lends the loan it will report $5000 as expenses in its financial statements. The remaining $95,000 will be reported as assets in the balance sheet.

If the default amount is more the provision made by the bank, then the bank will write-off that amount from receivables and will also report additional expenses. For example, if the default amount says $10,000, $5000 more than the provision for the bad debt. Then the bank will report an additional $5,000 as the expense and will also remove the entire amount.

When the bank writes off the non-performing asset, it receives the tax deduction for the loan amount. Moreover, even the loan is written off, the bank has the option to pursue the loan and generate some revenue from that bank. The banks also avail the option of selling the defaulted loans to third-party agencies to recover those loans from the customers.

Banks around the world are still under pressure due to the subprime crisis that affected the banking system. The customers took the loan for their house in lieu of mortgaging the house and could not return the loan. These loans needed to be written off form their balance sheet and as a result, put a lot of pressure in the financial health of the bank. The similar situation has happened in India as well where banks mainly public sector banks have lend money to organizations which have defaulted their loan payments. This situation resulted in writing off the loans from the balance sheet, resulting in shrinking of the book value of the banks.

Final Thoughts

Whenever a company has to write-off asset faces its impact on the future flow of revenue, as the asset can no longer generate any source of revenue for the company. But in spite of that, a company needs to write-off asset which is no longer in use for the company, as it helps the company to become cleaner and also avoid the situation of that asset using resources of another productive asset.

Tangible Assets Definition – “Any physical assets owned by a company which can be quantified with relative ease are usually known as tangible assets”.

These can include any kind of physical properties such as a piece of land which might be owned by a company along with any structure built upon it, including the furniture, machinery, and equipment housed in it, which is being used to carry out business operations.

List of Tangible Assets Examples

Property, Plant, and Equipment (PP&E) are long-lived tangible assets used in the production or sale of other assets. Cost of PP&E includes all expenditure (transportation, insurance, installation, broker cost, search cost, legal cost) that are necessary to acquire and ready them for use. If the plant is constructed, all the material, labor cost, overheads, interest cost during construction included in the Cost of PP&E.

Below is the list of Tangible assets examples

Property – Property includes the land, building, office furniture etc

Plant – Plant is the physical space where the workers work or provide services

Equipment – This refers to the machinery, vehicles and other tools & equipment used to produce

Inventory – This includes all types of inventory like the finished goods as well as WIP and raw material inventory

Tangible Assets Examples in Companies

Depending on the type of the company these assets may or may not make the largest asset amounts. Here are the two tangible asset examples –

High Capex companies like Oil and Gas companies, Real Estate Companies, Car Manufacturers have a large percentage of total assets tied up in Plant, Equipment, and Machinery. Therefore, you will find a large amount of tangible assets on the balance sheet.

Services companies like Microsoft or Infosys will have far fewer assets. Such companies own a large number of intangible assets like patents, copyrights etc.

Difference Between Tangible Assets and Intangible Assets:

Another type of assets which could be owned by a business is classified as intangible or non-physical assets, which can be difficult to quantify. These can include any trademarks, copyrights, and patents as part of the intellectual property owned by a business. Intangible assets goodwill and brand recognition are also often considered as part of intangible assets, for which there is no specific measure and can only be evaluated subjectively.

It is obvious how intangible assets goodwill differs from such assets in the very manner they manifest, and thus must be considered separately for all practical purposes. For instance, physical assets are typically vulnerable to wear and tear, might be damaged or stolen and are thus often liable to any form of losses or reduction in their value as a result of the same.

Intangible assets goodwill are more or less immune to physical damage in any form, but their value could be affected in other ways, for instance, brand recognition or brand equity of a business could be badly affected by gaining bad popularity over a spurious, faulty or damaged batch of products produced by a business. It could be quite difficult to assess the extent of damage to brand equity which might be caused due to such an event.

How are Tangible Assets Valued?

VALUE OF TANGIBLE CURRENT ASSETS:

The potential total cost of tangible current assets usually includes not only the amount for which it is purchased, as recorded in the relevant invoice as part of the inventory bought, but also includes any additional costs incurred due to transportation, for its installation and for insurance purposes as well.

VALUE OF TANGIBLE FIXED ASSETS:

As already discussed, tangible fixed assets have their value spread over its expected lifespan instead of being accounted for only in the year when they might be purchased. A part of their value is being accounted for every year in the accounts of a firm, known as depreciation, which also stands for the monetary worth reduced after a certain period of use.

Conclusion:

Tangible assets form an integral and important part of assets owned by a business and play a critical role in carrying out business operations effectively. They way their worth might be calculated might be a matter of consideration, however, as fixed assets are depreciated over time and depending on the method of depreciation adopted, the figure could vary from one business to another. Then again, such assets have to be separated from intangible ones to be able to evaluate and measure their worth with any amount of accuracy and this is exactly what net tangible assets is all about.

Having said that, the relevance of measures associated with tangible assets obviously have their limitations due to the difference in levels of intangible and tangible assets for different industries. Certain industries tend to have greater intangible assets goodwill and hence a lower number associated with net tangible assets would not represent the real picture while assessing a company from an asset-based perspective. Keeping all the possible uses and limitations in mind, tangible assets and related measures can be employed with good effect.

A sunk cost is an expense that has been already done and cannot be recovered. It is also known as stranded cost or retrospective costs or unrecoverable expense. When sunk costs are higher it creates a wall to the entry of new firms since they risk huge losses if the companies decide to leave the market. Since these kinds of costs cannot be recovered or regained they shouldn’t be considered while making rational decisions.

Examples of Sunk Costs

Let us discuss a few examples of sunk costs:

A company spends $50,000 on ma arketing study of its new product to see whether the new product will be a success in the market. The study concludes that the new product will not have a good run in the market. Then the $50,000 becomes a sunk cost and the company should not invest more in the new product project.

A company invests $20,000 to provide training to its staff in the use of new technology I the office which will be used in taking new complaint requests. The technology while using could not handle the complaint volume and is often taking faulty requests so the company decides to discontinue their use. This training is taken as the sunk cost and should not be taken into consideration while decision making.

A company pays $5000 as a joining bonus to a new recruit in the organization. After recruitment, it is seen that the employee’s performance is not up to the mark and he needs to be given the pink slip. Then this $5000 is taken as a sunk cost as this cost cannot be recovered.

In today’s world companies use advertising to attract new potential customers as well as retain the older ones. They use the different type of media like the print or audiovisual media to help in mass advertising. This advertising doesn’t promise any positive return but if the money is spent once on advertising and the advertising campaign is running then the advertising expenditures are called sunk costs.

If a company dealing with a specialized product that they only offer purchases equipment then this purchase of equipment is considered as sunk cost fallacy this equipment cannot be sold in order to regain money.

If a company hires an SEO specialist or marketing consultant to boost its business then they have to pay a service fee beforehand for the services provided by the consultant even before the work is done. The company does not have any provision to check the sunk cost effect of the services before the work is done and whether the consultant has made any positive difference to the business. This service fee then becomes a sunk cost fallacy since the money is spent already and it cannot be recovered even if the company dislikes the services of the marketing consultant or the SEO specialist.

What is Sunk Cost Fallacy?

Sunk cost fallacy happens when a business decides to continue its spending because of the pet decisions involved like time, money and resources instead of taking a rational decision and following choices which will maximize the returns in that time.

Sunk cost fallacy costs the business greater financial losses. It is human nature to think that once a cost has been made for a project or invested in a product it is better to invest more money even if the project or product is not a profitable one and is going to make losses.

For example, many individuals order too much food and then they overeat just to get their money’s worth. When factoring the costs of any exchange people tend to focus more on what they are going to lose in the bargain than on what they stand to gain.

Whenever businesses tend to cling to its costs because of the past time, money and resources already involved and take decisions based on that then this situation leads the business right into the sunk cost fallacy. This is also called Concorde fallacy describing it as an escalation of commitment.

Final Thoughts

Every organization faces the dilemma of sunk cost while decision making at some point. This costs cannot be avoided at any cost. Since these costs are in the past companies should not keep pouring money in these losses. Instead, companies must focus on the current market and ignore the previously spent costs. If there is no potential then they should stop investing and end the operations. We all don’t like losing money but letting go of the past in these situations can help in avoiding more losses in the future.

The petty cash book is a formal summarization of petty cash expenditures, sorted by date. In most cases, the petty cash book is an actual ledger book, rather than a computer record. Thus, the book is part of a manual record-keeping system. There are two primary types of entries in the petty cash book, which are a debit to record cash received by the petty cash clerk (usually in a single block of cash at infrequent intervals), and a large number of credits to reflect cash withdrawals from the petty cash funds. These credits can be for such transactions as payments for meals, flowers, office supplies, stamps, and so forth.

A somewhat more useful format is to record all debits and credits in a single column, with a running cash balance in the column furthest to the right, as shown in the following example. This format is an excellent way to monitor the current amount of petty cash remaining on hand.

Sample Petty Cash Book (Running Balance)

Date

Purchase/Receipt

Amount

Balance

4/01/xx

Opening balance

$250.00

$250.00

4/05/xx

Kitchen supplies

-52.80

197.20

4/08/xx

Birthday cake

-24.15

173.05

4/11/xx

Pizza lunch

-81.62

91.43

4/14/xx

Taxi fare

-25.00

66.43

4/23/xx

Kitchen supplies

-42.00

24.43

When the amount of petty cash on hand declines to near zero, as is caused by withdrawals for various expenditures, the petty cash clerk then obtains additional cash from the cashier, and records this cash influx as a new debit. The petty cash clerk also turns in a copy of his or her petty cash book to the general ledger account or cashier, who creates a journal entry to record how the cash in the petty cash drawer was used.

The petty cash book is a useful control over petty cash expenditures, since it forces the petty cash clerk to formally record all cash inflows and cash outflows. To ensure that this is an effective control, the petty cash book should be reviewed periodically by an internal auditor to see if the net total amount of cash available as per the book matches the actual amount of cash on hand in the petty cash drawer. If not, the petty cash clerk may require additional training.

The petty cash book has declined in importance, as companies are gradually eliminating all use of petty cash, in favor of using company credit cards.